California's Repossession Laws for Leased Automobiles

California’s laws relating to the repossession of leased automobiles are generally not as favorable to the consumer as the laws governing the repossessions of purchased cars and trucks. However, you still have rights. In particular, be sure to read the section below about the notice that must be sent to the consumer before the vehicle is sold at auction. If the leasing company fails to comply with the notice requirements, then it will be prohibited from attempting to collect the remaining lease balance from you. Accordingly, it is something that everyone viewing this page should read.

California’s laws relating to the repossession of leased automobiles are generally not as favorable to the consumer as the laws governing the repossessions of purchased cars and trucks. However, you still have rights. In particular, be sure to read the section below about the notice that must be sent to the consumer before the vehicle is sold at auction. If the leasing company fails to comply with the notice requirements, then it will be prohibited from attempting to collect the remaining lease balance from you. Accordingly, it is something that everyone viewing this page should read.

Important: if you leased a Mercedes-Benz automobile that was repossessed by Mercedes-Benz Financial Services, then read this Website’s Mercedes-Benz Lease Repossessions page to learn important information about the possibility of having your deficiency balance eliminated.

If you purchased your car or truck, instead of leasing it, then you should click on this link and read our page on the repossession rules for purchased cars and trucks.

Your Car Cannot Be Repossessed Unless You Are in Default

The first, and most important, repossession rule in California is that the leasing company or dealer cannot repossess your car unless you are in default under your lease. The most common types of default that result in automobiles being repossessed are either that the owner is behind on his or her payments or failed to maintain the required insurance coverage. If neither or these applies, and your car was still repossessed then you probably have a claim for conversion (i.e., civil theft) and/or unfair debt collection.

If your leased vehicle was repossessed even though you were current on your monthly payments, then you should immediately call an attorney who specializes in repossessions and consumer law to discuss your legal rights.

The Vachon Law Firm offers free consultations in wrongful repossession cases. Call us today at 1-855-LEMON-LAW (1-855-453-6665) to learn about your legal rights!

No Right to a Grace Period or to a Notice of Default

Under California law, consumers who fall behind on their lease payments are not entitled to any “grace period.” This means that a lender can repossess your vehicle even if you are only one day late on your payments. As a practical matter however, leasing companies tend to wait at least a month before repossessing a leased car or truck – but this is only because they want you to continue with your lease. There is nothing legally stopping them from repossessing your car if you are not up to date on your payments.

Under California law, consumers are also generally not entitled to any notice or warning that the leasing company or bank is going to repossess their automobiles. The only exceptions to this rule are (1) if the leasing company has told you (preferably in writing) that it will allow you to make a late payment (or payments), or (2) if the company’s prior practice led you to believe that the company would not repossess the vehicle. An example of the latter would be a scenario in which a consumer for six months in a row made all of his payments two weeks late. If the leasing company did nothing in response to these repeated late payments, then the consumer would have a strong argument that the company’s conduct led him or her to believe that it would wait at least to two weeks prior to repossessing one of its leased automobiles.

No Right to Redeem or Reinstate the Lease After Repossession

When a leased car or truck is repossessed in California the consumer generally does not have a legal right to reinstate the lease (i.e., to pay the overdue payments and repossession charges, and then get the vehicle back and continue with the lease). Similarly, if the leasing company terminates the lease contract because of late payments, then the consumer is usually also without a legal right to redeem the vehicle (i.e., to payout the lease by purchasing the car). That being said, leasing companies are virtually always willing to allow consumers to become current on their leases or to buy them out. So if you want to do either, you should contact the company immediately to make your request.

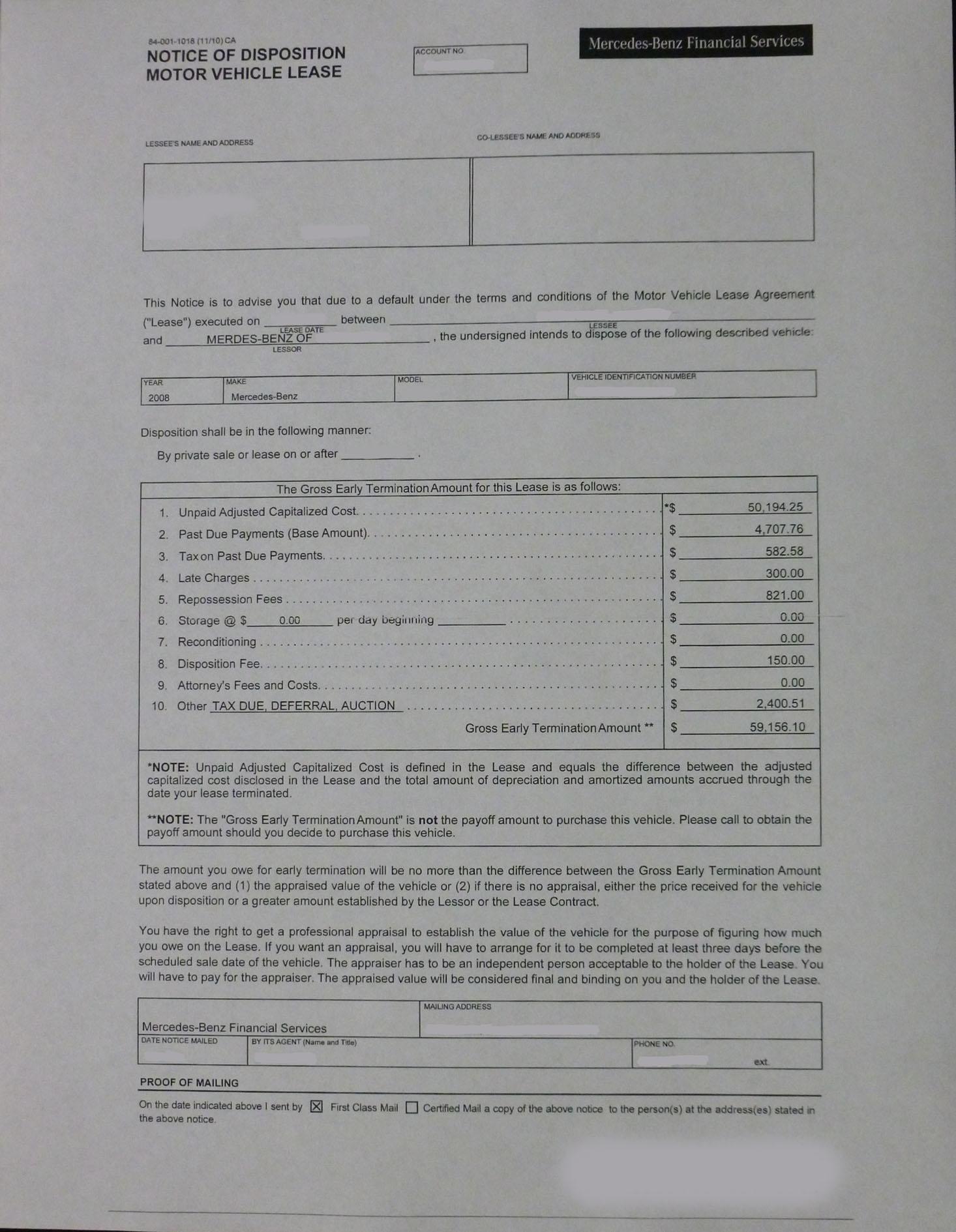

The Leasing Company Must Send You a Notice Prior to Selling Your Vehicle – Or it Loses the Right to Collect the Lease's Balance

California law requires that, at least 10 days prior to selling your repossessed vehicle at auction, the leasing company must send you a notice that informs you of the date on or after which it intends to sell your vehicle. The notice can be sent in the mail, but must be sent to your last known address. Accordingly, if you have moved since you leased your automobile, you should call the leasing company immediately and give them your new address to make sure that you get the notice.

The notice essentially contains an itemization of the total amount that you will owe under the lease, with the total to be reduced by whatever money the leasing company receives for selling your vehicle at auction. California’s laws governing these notices are very strict. In fact, if the leasing company makes any significant mistakes in the notice, then it will likely be prohibited from collecting the lease’s outstanding balance from you.

Click below to see a sample California post-repossession notice for leased automobiles:

The charges and amounts listed in this notice are calculated using financial amortization models, and are accordingly too difficult for most consumers to understand. However, leasing companies often make mistakes in these calculations – and you should definitely show your notice to an attorney who specializes in lease repossessions to make sure the leasing company calculated it correctly.

The Vachon Law Firm reviews repossession notices for free. Call us at 1-855-LEMON-LAW (1-855-453-6665) today, and we will look over your repossession notice at no charge.

You Have a Right to Pay for an Appraisal Rather Than Have the Vehicle's Value Determined at Auction

The pre-sale notice that the leasing company sends after it repossesses a leased automobile must state that you that you have a right to have the vehicle’s value determined by an appraisal, conducted at your expense, rather than having the value determined at auction. Although paying for an appraisal is the last thing that most people want to do after someone repossesses their car, it is something you should seriously consider. Although the price of an appraisal is likely to be a few hundred dollars, if the vehicle is sold at auction it will likely sell for 5% – 20% below its fair market value. If you can afford to pay for the appraisal, it may save you hundreds or thousands of dollars in the long run.

Contact an Attorney to Discuss Your Repossessed Vehicle

The Vachon Law Firm offers free consultations in lemon law, car dealer fraud, and repossession cases. If you have questions about your repossession, then call us today at 1-855-4-LEMON-LAW (1-855-453-6665).

We’re here to help!

- Back to California Lemon Law Page

- Back to Home Page